Invest Smartly: Understanding Future Value of Investments and the Impact of Inflation

In today’s fast-paced financial world, we often hear advice on investing wisely, but not all of us fully comprehend how different investment modes stack up against each other. A common question is, “Where should I invest my money for the best returns?” But equally important is asking, “How will inflation affect my returns in the future?” The answer to this requires understanding how various asset classes—cash, bank accounts, fixed deposits, mutual funds, and shares—grow over time and the real returns they generate when adjusted for inflation. In this blog, we explore how different investments grow over time and how their inflation-adjusted value looks, using an example of investments in 2024 and their projected value in 2034.

1. The Effect of Inflation on Your Money: A Silent Killer

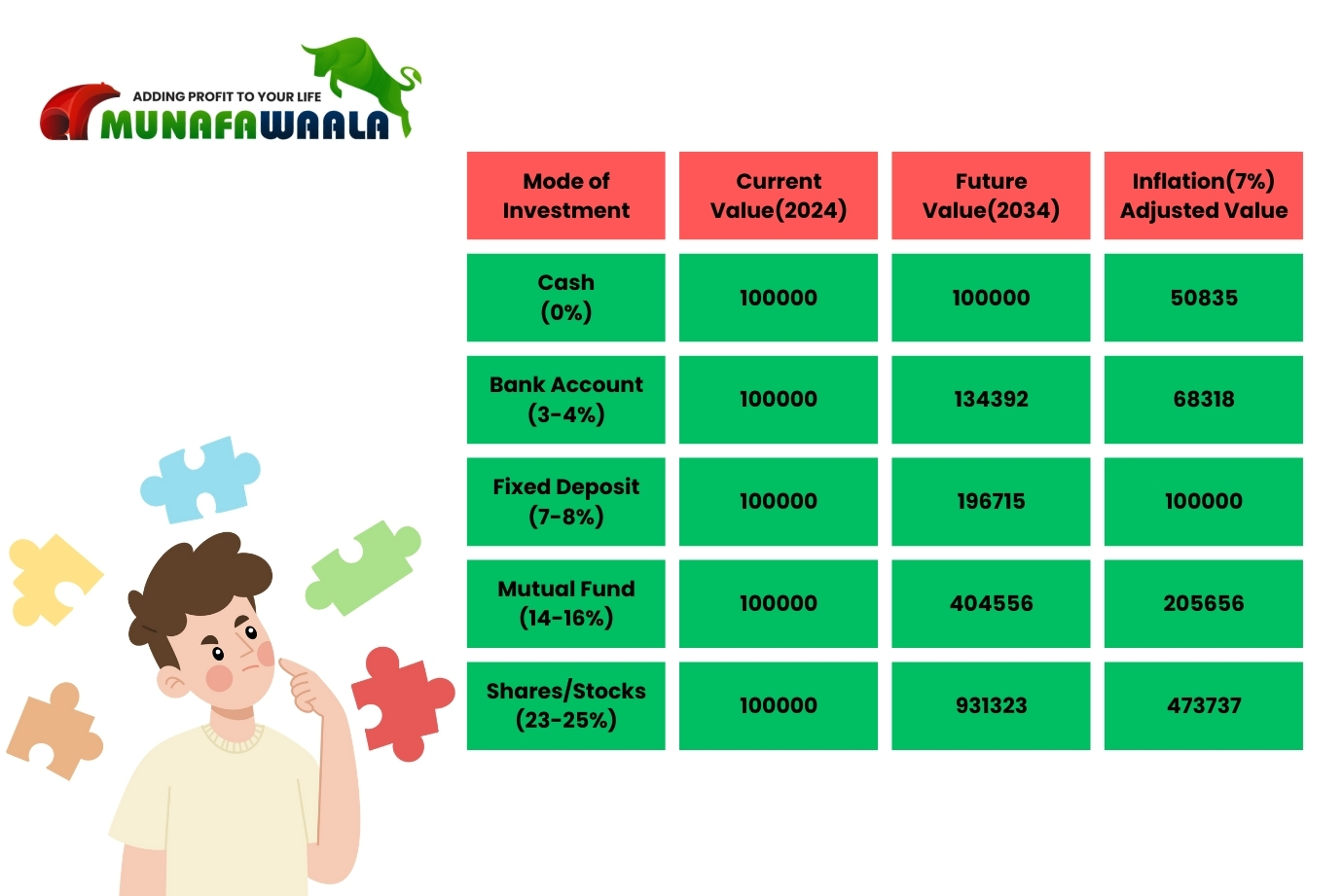

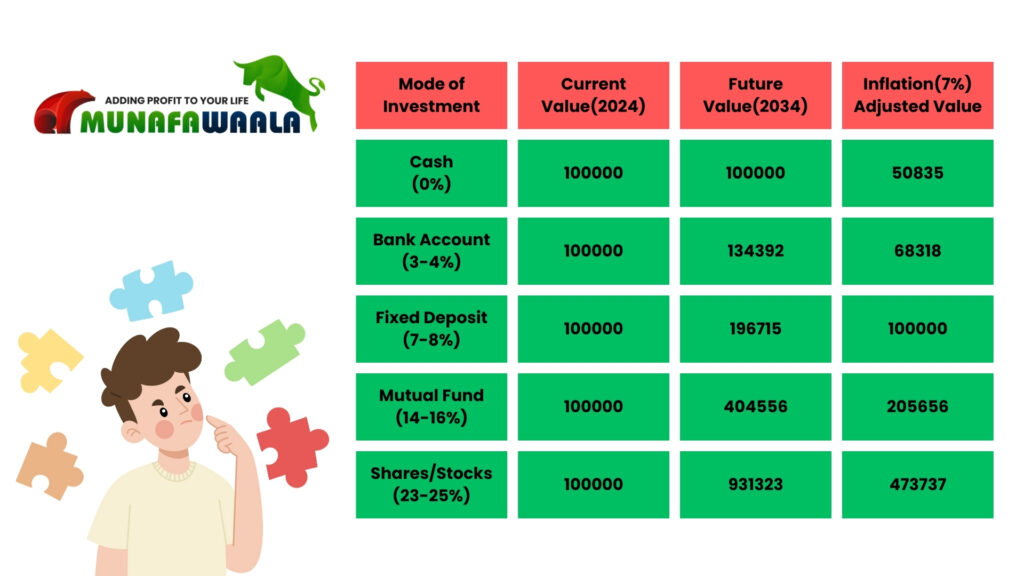

Inflation, the rise in the general price level of goods and services over time, directly impacts the purchasing power of your money. While you may feel secure seeing your wealth grow over the years, inflation eats away at that growth. For instance, if inflation is 7% annually, your ₹1,00,000 today will only have the purchasing power of ₹50,835 in 10 years. Therefore, it is critical to consider inflation when planning long-term investments.

2. Investment Modes: Understanding the Basics

To understand how inflation and investment returns interact, we can analyze five common investment options:

- Cash (0% return)

- Bank Account (3-4% return)

- Fixed Deposit (7-8% return)

- Mutual Fund (14-16% return)

- Shares/Stocks (23-25% return)

Each of these investments grows at a different rate, and the future value in 2034 will vary depending on the type of asset. However, the inflation-adjusted value is crucial in determining how much your wealth is truly worth in real terms.

3. Cash (0% Growth): The Worst Offender

Let’s start with cash. If you leave your ₹1,00,000 in cash under the mattress, its future value in nominal terms will remain ₹1,00,000. However, inflation dramatically reduces its real purchasing power. After 10 years, with 7% inflation, its inflation-adjusted value will drop to just ₹50,835. This means that the same ₹1,00,000 will buy you only half of what it can buy today. Holding onto cash for long periods is a sure way to lose purchasing power over time.

4. Bank Account (3-4% Growth): A Safe but Low-Return Option

Many of us keep our savings in a bank account, which typically offers an interest rate of 3-4%. Using the same initial amount of ₹1,00,000, the future value at 3.5% interest will be ₹1,34,392 in 10 years. While this looks like a decent increase, inflation reduces this significantly. The inflation-adjusted value in 2034 will be ₹68,318, barely an improvement over today’s purchasing power. Though safer than keeping cash, savings accounts barely help combat inflation, making them suitable for short-term goals but inadequate for long-term wealth building.

5. Fixed Deposit (7-8% Growth): A Moderate Return with Safety

Fixed deposits (FDs) offer a return of 7-8%, which is higher than savings accounts but still might not keep up with inflation. A ₹1,00,000 investment in 2024 will grow to ₹1,96,715 at 7.5% interest after 10 years. Inflation reduces the real value to ₹1,00,000, meaning the purchasing power of your FD remains the same over time. This makes fixed deposits a relatively safer option for those seeking capital protection, but you’ll break even only when considering inflation.

6. Mutual Funds (14-16% Growth): Balancing Risk and Reward

Mutual funds provide an opportunity to participate in the market’s growth, offering higher returns of 14-16% over time. For our analysis, let’s take an average return of 15%. In this scenario, your ₹1,00,000 grows to ₹4,04,556 over 10 years, giving you substantial nominal gains. After adjusting for inflation, the value is ₹2,05,656, which is significantly higher than other conservative options. Investing in mutual funds, especially equity-oriented funds, helps grow wealth over time despite inflation, making them ideal for long-term goals such as retirement or children’s education.

7. Shares/Stocks (23-25% Growth): High Risk, High Reward

For those who have a higher risk tolerance, investing in individual stocks can provide exceptional returns, ranging between 23-25%. Based on this range, a ₹1,00,000 investment grows to ₹9,31,323 over 10 years at a 24% rate of return. Even after adjusting for inflation, the inflation-adjusted value stands at ₹4,73,737, which is far above the returns from any other investment type. While stock markets can be volatile in the short term, history shows that long-term equity investments tend to deliver superior returns, making them a good choice for investors with a long investment horizon and the ability to stomach short-term fluctuations.

8. Choosing the Right Investment Based on Your Goals

The key takeaway from this comparison is the importance of investing in assets that at least beat inflation. While fixed deposits and bank accounts provide safety, they may not offer enough return to grow your wealth meaningfully when adjusted for inflation. On the other hand, mutual funds and stocks provide the potential to grow your money significantly, even after accounting for inflation, making them ideal for long-term wealth creation.

Before choosing an investment path, it’s crucial to align your choices with your financial goals and risk tolerance. If your priority is preserving capital with minimal risk, then FDs and savings accounts might work for you. However, if you want to build substantial wealth over the long term and beat inflation, mutual funds or stocks should be part of your portfolio.

9. The Role of Diversification in Beating Inflation

One of the best ways to mitigate risk while still aiming for higher returns is diversification. Instead of putting all your money in one investment type, spreading it across different asset classes such as fixed deposits, mutual funds, and stocks can help balance risk and reward. By diversifying, you ensure that even if one asset underperforms, others in your portfolio may compensate and keep your overall wealth growing.

10. Consulting a Financial Advisor for Tailored Advice

It’s important to note that each person’s financial situation, goals, and risk appetite are different. What works for one may not work for another. Therefore, consulting with a financial advisor like Munafawaala can help you make informed decisions tailored to your specific needs. Whether you need guidance on mutual fund investments, tax-saving strategies, or insurance, Munafawaala can provide personalized advice to help you achieve your financial goals and ensure that inflation doesn’t erode your wealth over time.

Conclusion: Don’t Let Inflation Rob You of Your Future

The journey to building wealth is not just about how much money you make but also how much purchasing power you retain in the future. As seen in the comparison across various asset classes, inflation can dramatically reduce the value of your money if you do not invest wisely. Therefore, to achieve long-term financial goals, it’s essential to invest in assets that can outpace inflation, such as mutual funds and stocks. At Munafawaala, we are dedicated to helping you make informed investment choices to grow and protect your wealth for the future.